BlackScholes-Delta

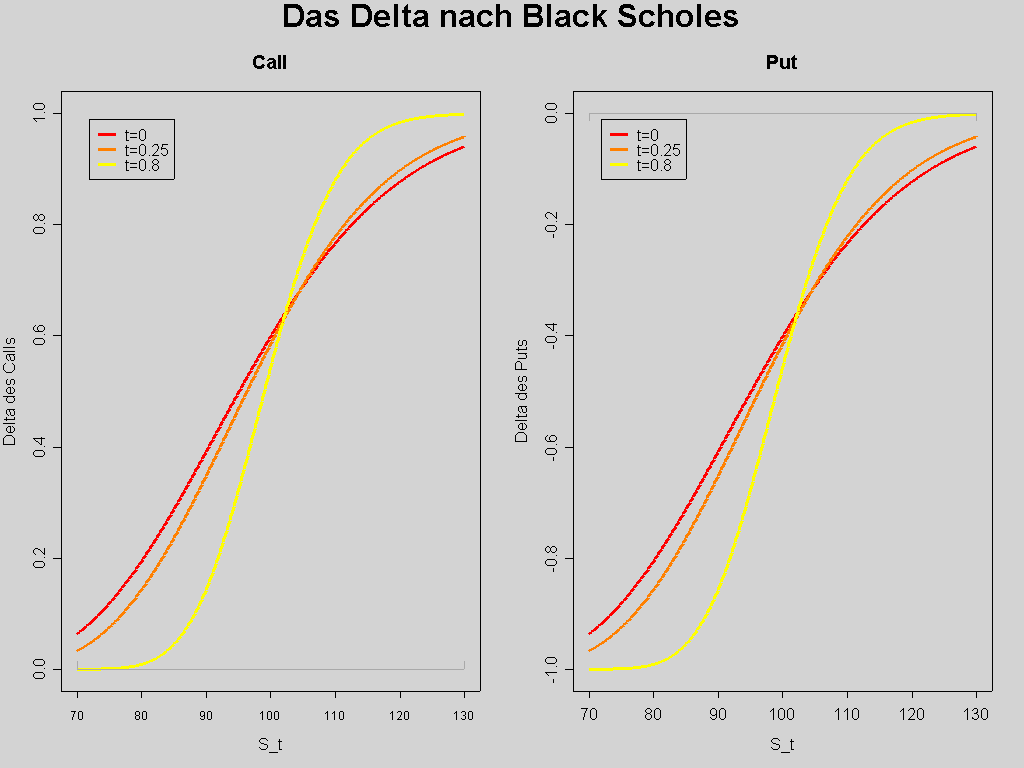

selbst erstellt mit GNU R. R-Quelltext: bsDelta <-function (flag="c",S,t=0,T=1,K=100,sigma=0.20,r=0.03) { d1=1/(sigma*sqrt(T-t))*(log(S/K)+(r+sigma^2/2)*(T-t)) d2=d1-sigma*sqrt(T-t) if (flag=="c") { return(pnorm(d1)) } else if(flag=="p") { return(-pnorm(-d1)) } } cols=heat.colors(3) s=seq(70,130,length=500) png(filename = "BlackScholes-Delta.png", width=1024, height=768, pointsize = 12)

par(mfrow = c(1,2), oma = c(0,0,2,0), bg="lightgrey") plot(s,bsDelta(flag="c",S=s,t=0,T=1),type="n",ylim=c(0,1),xlab="S_t",ylab="Delta des Calls") lines(s,bsDelta(flag="c",S=s,t=0,T=1),type="l",lwd=3,col=cols[1]) lines(s,bsDelta(flag="c",S=s,t=0.25,T=1),type="l",lwd=3,col=cols[2]) lines(s,bsDelta(flag="c",S=s,t=0.8,T=1),type="l",lwd=3,col=cols[3]) axis(3,pos=0,labels=FALSE,col="darkgrey",at=c(70,130)) legend(x=72,y=0.99,legend=c("t=0","t=0.25","t=0.8"),col=cols,lwd=3) title(main="Call")

plot(s,bsDelta(flag="p",S=s,t=0,T=1),type="n",ylim=c(-1,0),xlab="S_t",ylab="Delta des Puts") lines(s,bsDelta(flag="p",S=s,t=0,T=1),type="l",lwd=3,col=cols[1]) lines(s,bsDelta(flag="p",S=s,t=0.25,T=1),type="l",lwd=3,col=cols[2]) lines(s,bsDelta(flag="p",S=s,t=0.8,T=1),type="l",lwd=3,col=cols[3]) axis(1,pos=0,labels=FALSE,col="darkgrey",at=c(70,130)) legend(x=72,y=-0.01,legend=c("t=0","t=0.25","t=0.8"),col=cols,lwd=3) title(main="Put")

title(main="Das Delta nach Black Scholes", cex.main=2, outer=TRUE)

dev.off()

Relevante Bilder

{kind=link}

Relevante Artikel

Black-Scholes-ModellDas Black-Scholes-Modell ist ein finanzmathematisches Modell zur Bewertung von Finanzoptionen, das von Fischer Black und Myron Samuel Scholes 1973 veröffentlicht wurde und als ein Meilenstein der Finanzwirtschaft gilt, siehe Abschnitt Preisformeln für das Ergebnis. .. weiterlesen